(User manual: This is a really long article. Should we come across something like this ourselves, even though we do have concern for the environment yet for the health of our own eyes as well, therefore we would probably print it, and read it afterwards. This is however a question of one’s endurance. At the same time, the article is fitted with extensive graphic content, evidently best accessible through a computer, so keep one close at all times. At graphic visualizations it is worth clicking around a little bit as they are all based on an enormous database and consequently they contain much more information under the surface. We did our best to feature data that we think is the most interesting but further numbers and graphs are available by clicking on the other tabs. Thanks to the advanced technology, all these graphs are made individually shareable and embeddable. Have a nice read!)

Foreword

The following pages will analyze changes in the advertising and media market that happened under the second Orbán-government. The enquiry will try to answer the following questions: who are those running the system after the change of governments, how public tenders of the communication sector became distributed after 2010, and who were the beneficiaries of the system on the advertising and media market.

The media war erupting in the past weeks as well as the ruptures becoming visible in Lajos Simicska’s media empire could raise the issue of whether it is sensible to deal with this topic now? We will describe system that fall into pieces after the formation of the third Orbán-government or a few weeks ago at the latest. This seems like a question with a point. We think however that firstly presenting the establishment and the functioning of such a system could be helpful, so that a similar exposure and distortion of the Hungarian media on that level would not happen again. Secondly, in this way during the following years, names and personalities mentioned here could be reminded of and confronted with what they have taken part in between 2010 and 2014.

During this time we could have seen the establishment and a full-throttle functioning of such a machinery that shows an unprecedented plan of central organization of players and duties. The whole process was more or less apparent not only for market stakeholders and people interested, but due to recurrent reports published in nationwide news sites, to the wider public was informed about major changes as well. The whole system however was unable to be exposed for any fallacies as in the overwhelming majority of the cases everything went down following the law, and often surrounded by the passivity of market competitors.

How a process like this could be executed undisturbed? What was preventing agencies from applying to open public tenders and to challenge preferred agencies? Why the Hungarian media market was tacitly assisting the disproportionate spending of public advertising money by the state in way that was mainly out of the rules of market metrics? Our study will aim to answer these questions following this structure:

- The history of the establishment of Fidesz’s media empire

- Key figures in running the media empire

- The winners of media-acquisition public tenders

- The distribution of state advertisement

- Beneficiaries of the system

- Recommendations for a way out

Part I.

THE ESTABLISHMENT OF THE FIDESZ MEDIA EMPIRE

After the change of regimes in 1989 a need for balancing the Hungarian media market with the help of a state intervention on behalf of a rightist government has increasingly been articulated as a demand on the political Conservative-Right. They thought that post-1989 privatized media market preferred the leftist-liberal political parties through changes in owner structure and in “ideology.” This view, mostly being carried by the radical right in the first years of the nineties has been endorsed by Viktor Orbán and appeared in Fidesz following his Conservative-rightist turn. After being elected in 1998, it became one of the primary objectives of the party’s media policy by the end of the year. With their first steps, they reinforced daily print Magyar Nemzet, and established the Conservative weekly print Heti Válasz. This was soon to be accompanied by the traditional pro-government stand of the public media as well as the public sphere domination of outdoor billboard company, Mahir Cityposter that were already in the possession of Fidesz financial strongman Lajos Simicska.

The 2002 election defeat however raised serious question within Fidesz in connection with the underestimation of the role of the media in the previous government term. In fact that was the time when Fidesz realized that besides print media, they need a much more complex and effective media portfolio. As a first step they established Hír Television using donations and investments from rightist businessmen, and in September 2005, pro-Fidesz oligarch Gábor Széles started his own cable channel, Echo Television. He also acquired daily print Magyar Hírlap, turning it into a forum often sympathizing with far-right political views in the course of six months.

In the run-up to the downfall of the left and the liberals in the 2010 elections a lot of movement on behalf of Fidesz’s financial hinterland was going on the media market. They acquired two additional billboard companies (Publimont and Euro Publicity) and divided national commercial radio frequencies between themselves and the Socialists following what could be called one of the most scandalous mediapolitical pact of the history of post ‘89 Hungary. In a process that later has been deemed by the court to be illegal, these frequencies were granted to Class FM, owned by Zsolt Nyerges, one of the strongest pro-Fidesz businessmen, while Socialists had connections to the now defunct Neo FM.

After this, Károly Fonyó, a businessman with close relations to Lajos Simicska since the 1990’s, bought free handout daily journal Metropol in 2011 from its publisher, the Swedish Modern Times Group. With this Fidesz not only achieved “ideological” but also financial domination with its media portfolio at the time consisting of five outdoor/billboard companies (Publimont, Mahir Cityposter, EuroAWK, Euro Publicity, A Plakát) a national and a Budapest-local commercial radio station (Class FM, Music FM) three daily papers (Metropol, Magyar Nemzet, Magyar Hírlap) two weekly papers (Heti Válasz, Demokrata) two televisions (Hír TV, Echo TV) completed with the entire public media (M1, M2, Magyar Rádió, MTI News Service, Duna TV). Such a strong media portfolio has also been joined by others as co-travellers. These according to their owners cannot be directly connected to the classic Fidesz-oriented media, based on their informing practices and other connections however they can be classified as allied or rightist media (TV2, Helyi Téma). A series of rightist online media publications (MNO, Pesti Srácok, Tutiblog and the defunct and revived OXOX) later were a completion to the process.

This media empire could not have been established without the profound financial contribution of Fidesz-oriented businessmen. But the portfolio needed to be operational, as well as profit-generating. For this, the media empire had to overcome a number of difficulties. Recession following the 2008-09 economic crisis cut Hungarian advertising market almost by third, and certain elements of the portfolio were either too new or too weak to become attractive for commercial advertisers. By 2010-11 it became entirely apparent, that without a significant intervention from the state sector, these media enterprises are not only impossible to become profitable, but it would also face operational disturbances.

Consequently, the Hungarian state and the players started to make the system financially operational following multiple methods. The most important of these was channeling state advertisement money to the friendly media. In this process, some media advertisement agencies, like IMG, Vivaki Group, Bell & Partners and Initiative Media played a key role (see an elaboration of this point further below.)

The two-thirds majority legislative assembly helped to make functioning for some market competitors impossible (see the “Lex Mahir”, advertisement tax and its amendments). The competition regulatory body did not deal with grave issues arising from the conflicts of interest within Fidesz’s media empire, meaning the fact that the majority of media- and advertising key figures are connected to the same interest group. Media Authority helped to clean the radio market up for Class FM. In the meantime, representatives of the government first started to systematically attack private media companies (like Sanoma, Axel Springer’s Világgazdaság, Origo, Index, RTL Klub). The whole process was more or less tacitly observed by the official representation of the communications trade, who only stood up against Fidesz immediately after its 2014 reelection when plans of an advertising tax surfaced.

Classic theories of press freedom measure the diversity of information with the plurality of the ownership structure present at the media market. More plurality in the ownership structure means more diversity in the sources of information. These classic theories presume that everyone “has the opportunity” to access information, and plural ownership structure is per se ideal, and therefore a diverse ownership structure results in a situation where “anything can be printed.”

Following the 2010 change of governments a profound restructuring happened in this regard. The two-thirds majority passed legislation preventing transparency, and curbing not only the right to access information, but making source protection for journalists more difficult. State companies and agencies in connection with the state aimed to overwrite the Fundamental Law with the new Civil Code, Freedom of Information (FOI) requests routinely ended up as court cases, in many instances going as far as the Supreme Court (Curia), where the justice system usually ruled in favor of those requesting information, but the losing parties were reluctant to comply with the verdicts afterwards. The governing majority parallel to that started to cut the Information Act to size, making the accession of FOI data more and more difficult. On the other hand, media market actors independent from the government often presented an image of independence by cutting out political content in their programs, commercial advertisers were reluctant to place ads in media outlets that openly subscribed to a government-critical, or opposition point of view, even if their metric audience data would make advertising a logical choice. In 2014, Fidesz attempted to gain more influence in the online media market. A possible first step of such intentions could have been the dismissal of editor-in-chief Gergő Sáling from Origo while the government raised the possibility of imposing a severe internet tax as well. This would have made it financially much more difficult for the public to access the online media.

It is true that the ownership structure of the Hungarian media is diverse, but it’s far from ideal. In numerous cases, these owners have a connection to the government that is more of a financial than of an ideological nature. An example for this is Magyar Telekom that is interested in a number of state acquisition contracts as a communications service company. CEMP, publisher of Index is owned by Zoltán Spéder, who holds FHB Bank as well as Savings Associations Inc. in his interest group. One of the shareholders of Central Media Company, that is the owner of Hír24, Zoltán Varga, also has other interests outside the media market.

By 2014, barely any media actors remained on the market, who in themselves or through their owners would not have gotten too close to the state redistribution system during one government or the other. When the question of how the Orbán-government was able to restructure the balance of power in the media in such a short time, then we should always keep in mind that advertising and media market before the second Orbán-government was already entangled by political and economic backdoor deals.

We deemed this short overview necessary because without such a superficial summary of the background and antecedents, the complexity and simplicity with which the processes after 2010 unfolded could not fully be grasped. When you read certain chapters of this analysis, always take it into account, that even if a new era in terms of quality has started in the Hungarian media and advertising market, activities of the previous governments were essential in the fact that such a scenario could be realized.

The most important questions

Everyone is naturally most interested in whether the event could be classified as corruption, and how much money do we really talk about? Both question can be easily answered: hard evidence, documents, leaked emails, people involved giving quotes on the record are all missing. Of course there are detailed stories written down out of which intentions to exercise pressure or settle matters smoothly is apparent. But these are more like faulty strings in a well functioning machinery.

At the same time it can be realized using simple logic that there are fundamental models, and phenomena that could be observed quite often and that significantly increase the risk of corruption. These in themselves are no evidence to corruption but the more such patterns could be revealed, make the probability of a corrupt environment higher (to this please consult reports and studies prepared by Transparency International Hungary). In the system itself, corruption will reveal itself not in isolated cases but in an organized manner. According to the theory such risk factors include:

- Revolving-door effect: Certain people leaving the private sector immediately appear in state administration of government apparatus, where they will have significant influence on decisions and legislation if not they are the ones directly making such decisions. The opposite of this statement is also true: one could capitalize on his earlier state and government connections, social leverage and accessed confidential information in the private sector. In a more simple way: who are running the system, are who are those benefitting from it?

- State capture: In close connection with the revolving-door effect, the interlacement of the private and state sectors always result in a shared decision making process during which practices that earlier were illegal or irregular were being legalized to be applied for or against a market actor. But also, selective application of existing legislation by authorities and regulators (such as the Media Authority, the Competition Authority, the Authority of Procurements, state attorneys, investigative bodies) resulting in the positive discrimination of some and the negative discrimination of others, and also in tolerating cases suspicious of corruption, and sabotaging official duties. In a more simple way: how do operators and beneficiaries work together?

- Decreasing/low level of competition: is competition on the procurement market is decreasing, and furthermore the circle of tender winners are getting more exclusive, then the funds received will become more concentrated. Decrease in competition is usually a result of some competitors leaving the tender as a result of an external pressure, or of the recognition that they have no chance of winning public tenders. On behalf of the state steps taken to decrease competition included an intention to prevent an open procurement tender advertisement, or putting out tender applications with such conditions that fundamentally narrows down the circle of those eligible. A good example to the former practice is when a basic amount of money is being separated into smaller quantities that will not individually reach the threshold of a compulsory tender advertisement, so that they do not have to publicly advertise it. Or when the advertiser of a public tender does not classify the duty to fall under the auspices of the Procurement Act (PA) and advertises a simple tender. In the latter case it is a usual practice to announce a restricted procurement tender, inviting only pre-selected companies, or requesting references that only make these selected companies eligible.

Usually it is also suspicious when the deadline for application is extremely short. It is however tells much more than these tricks, when there is a mistake in the machinery, and a company not holding interests in the redistribution system participates in a procurement, decreasing the chances of the interested party to win. In case of such an event the announcer could call an end to the procurement as unsuccessful, or could exclude the party not holding interests for trumped-up reasons.

- Single direction cash flow: is when the route of concentrating public money is one-direction. This means that after observing the route of public money and identifying its end station reveals a group of interest consisting of the same people.

- Simulated competition: meaning that participants of a procurement process act like there is a real competition. It is also a very characteristic corruption pattern, when barely the same range of companies enter certain procurement competitions all the time. Even though the average number of these participants can be increased, creating an impression of competition, yet in reality all participant companies represent the same group of interest.

- Decreasing/low-level transparency/accountability: corruption on the state level could force participants to try and pass legislation that will decrease transparency and accountability.

- Narrowing opportunities of legal remedy: This could mean a rapid increase in the expenses of legal remedy due to a legislative amendment, or that as a result of a floating regulation the interpretation of the law by the authorities becomes flexible based on whether they would like to prefer or to sideline the applicant party.

Acknowledgements

At communication procurements, we worked with the Center for the Research of Corruption, Budapest (CRCB) lead by István János Tóth. A cleansed and ordered set of data referring to state sector advertisements is being acquired from Kantar Media market research company. An invaluable assistance in visualizing data has been offered to us by Rita Zágoni of the Microdata working group at Central European University. This series of articles would not have been possible without the journalists and researchers who uncovered the many anomalies of Hungarian advertisingt and media market in the past four years. This refers but not limited to Gergely Brückner (Figyelő), Gábor Csuday (ex-Kreatív), Gábor Ferencz (Átlátszó), Áron Kovács (ex-HVG.hu, VS.hu), Ildikó Kovács (Átlátszó), Ferenc M. László (HVG.hu), Babett Oroszi (Átlátszó, RTL Klub), András Pethő (ex-Origo, Direkt36), Gábor Polyák (Mérték), Pál Dániel Rényi (Magyar Narancs), Krisztina Rozgonyi (PPK Partners), László Sándor, András Szabó (VS.hu), Zoltán Szabó (Index), Gábor Tenczer (Index), Ágnes Urbán (Mérték), Balázs Weyer, and the whole editorial office of Kreatív.

Part II.

THE MEDIA SYSTEM OF NATIONAL COOPERATION

Part II of our article will introduce people who are playing key roles in the operation of the system in one way or another. These people, residing in different positions of public administration, top management of big state companies, decision makers of beneficiary agencies and media publications are profoundly connected to two circles of interest. The major circle is connected to businessmen Lajos Simicska and Zsolt Nyerges, and the other can be associated with two well-known personalities in and around Fidesz: Antal Rogán and Árpád Habony.

Two years ago, investigative online Átlátszó compiled the article: The System of National Cooperation (SNC): who captured the Hungarian state?, in which they featured all key figures mentioned in our present article. As a sub-project of this, we cooperated with Átlátszó to prepare a gallery of media personalities of SNC. However surprising this may be, it did not occur to us at the time to connect the dots between the two lists. However while we compiled a list of top managers of state advertising companies it immediately became clear that these people are the same as the most important figures in Átlátszó’s earlier article. It is not a coincidence either that none of these management figures could retain their positions after the formation f the third Orbán-Government, we will write more about the consequences of this at the end of our study.

State sector and administration

After the formation of the second Orbán-government, more and more people connected to the circle of Lajos Simicska and Zsolt Nyerges appeared at the top positions of state companies. This includes Kálmán Szentpétery at Szerencsejáték Zrt. (the company running among others the national lottery), Gergely Horváth at Magyar Turizmus Zrt., Zoltán Petykó at Nemzeti Fejlesztési Ügynökség (National Development Agency), Csaba Baji at Magyar Villamos Művek (Hungarian Electricity Works), Csaba Fazekas at Médiaszolgáltatás-támogató és Vagyonkezelő Alap (Media Service-Supporting and Assets Management Fund) and István Töröcskei at Államadósság-kezelő Központ (National-debt Management Center).

The two most prominent leaders of state offices regulating procurements were Róbert Gajdos heading the Procurement Office, and Zoltán Kövesdi leading the Procurement Decision Board responsible for settling debates, both were in connection with Simicska. The body regulating media with administrative measures, the National Media and News Authority is chaired by a former legal attorney of the Simicska empire, Monika Karas.

The topic of which agencies are connected to the Simicska-Nyerges group have been investigated and proven in the article by Átlátszó as well as the joint investigation of Átlátszó and Kreatív, therefore we will not detail this topic here.

The other group of interest within Fidesz’s media system is a circle much smaller than the former, thats main centre of power is the person of Árpád Habony, and this is where the Századvég-group can be found as well. This circle of interest did not build a huge media portfolio between 2010 and 2014, and its slow expansion can only be seen by the acquisition of economic daily Napi Gazdaság. HG 360 owned by Csaba Csetényi and Tibor Krskó is also an important actor of this circle, securing significant state communication agency contracts (Államadósság-kezelő, Magyar Turizmus, Hungarian National Bank).

As we can see from the disclosed network map, the system is extremely heterogenous yet not to the extent of being untraceable. The level of planning, arrangement and fluency within the system would suggest a masterpiece, but we should keep it in mind that this has not been set up for some noble cause, but for the sole purpose of turning public money into private money without the slightest risk of being exposed or accountability. How this whole system was successfully executed is the topic of our next chapters.

| How to use Tableau infographics? |

Tableau is a data visualization software that can be installed on our computer. With the help of the program we can prepare dynamic infographics embeddable into any website. Its main benefit compared to other softwares known to us is that it is extremely smart, allowing a great deal of liberty, and a high level of personalization while being able to handle and move a huge amount of data. Refreshing the database will also refresh the graphs while allowing a range of possibilities both to the reader and to the author. Even though figuring out how the program works can be easily achieved by a few clicks and moves with our mouse, we will hereby provide some hints for using it. On the graph going over the data points will result in a popup window showing detailed data information. We can also zoom into the graphs with a double click. We can also filter data by year, company or advertiser. If we left click on the “keep only” button, than the program will only sow one object we chose and every data referring to it. Clicking “exclude” button will take the chosen object out of the objects appearing, and it will disappear from the graph. There are some infographics that are wider than the text of the article by nature, we can follow them through by using the scroll of our mouse. It’s worth a look, because we can find the most stunning data there. If you have a slower configuration, don’t worry, it will only take some additional seconds to appear. There are some times, when you may feel like you have created a mess in the visualization as you don’t know how to return to the full visualization from the filtering. This is why it has an “Undo” (that undoes one step) feature as well as “Reset” function (that will take you back to the original). You can switch between infographics that are on the same graph body by using the small tabs. If your calculation was right, you can browse among 45 different infographics while reading the article. In addition you can share individual graphs at your preference! You can send a link to the graph, copy its embed code and download it both as a picture and a PDF document by using the “Share” function in the lower right corner. |

Part III.

CHANGES IN COMMUNICATION PROCUREMENTS (1.05.2010 - 30.04.2014)

Database sources: Közbeszerzési Értesítő (Procurement Digest), Tenders Electronic Daily, own collection

Methodology used to collect data: software downloading based on CPV numbers (numbers identifying the subject of procurements)

Systematization of data: Through Microsoft Excel. The data then was filtered and refined using Google Refine, to exclude duplications and procurements with an irrelevant subject, as well as unsuccessful procurement tenders.

Number of downloaded records: 1,584 lines (102,667 cells)

Number of clean and used records: 898 lines (4,494 cells)

Period of examination: May 1 2010 - April 30 2014.

Visualization software: Tableau Public

Do we publish raw data for double-checks? Yes we do.

Most important findings:

During the past government term, almost half of all communication procurement processes were distributed by the state sector either to one applicant or without a formal competition.

The more money at stake, the fewer applicants there were.

Almost two-thirds of all the state funds were received by three agencies: I.M.G., Vivaki and Bell & Partners.

Six out of the ten agencies/media outlets most successful on the state tenders, have a direct connection either with the pro-government economic hinterland or with the government itself.

Introduction

During government changes in Hungary, it usually can be observed that the circle of economic beneficiaries changes and reformulates. Political alternation of course is not something exclusive to Hungary, it is a well-documented phenomenon in Western Europe as well. The circle of beneficiaries at communication procurements does not necessarily coincide with the traditional political-ideological ambitions in most cases new figures emerge in the place of the old for the sake of a secure, confidence-based channeling of cash flow.

In order to analyze developments of political alternation, “procurement market” is one of the most ideal fields of investigation. The analysis of our data will reveal that winners of procurements in the the category of communications became completely replaced, and that competition decreased in an inversely proportional way with the amount of funds at stake parallel with the fact that greatest winners never really had to get their feet wet for success.

| The methodology of data collection |

Analysis was made in a joint effort with the Corruption Research Center of Budapest (CRCB). Basis of the analysis the Hungarian Database of Procurements (MaKAB) compiled by CRCB based on Hungarian Közbeszerzési Értesítő (Procurements Digest) as wells on Tenders Electronic Daily, the official digest of the European Union. We collected examined procurement processes based on their CPV number that is referring to the subject of the tender. This has been complemented by our own database with those state commissions that were sadly not published in either of these sources, and with those that to our best consideration should have been the subject of a public procurement process as public funds were spent to them. We only examined advertising campaigns that were complete with answers to at least four of the questions detailed as follows: When the results were published? Who was the announcer? Who was the winner? What was the subject of the tender? and How many applicants there were? We did not consider those commissions in which only the identities of the commissioner and the winner are public, but the budget handled by them and the number of competitors are not (for example: Hungarian Electric Works - Vivaki, Erzsébet-vouchers - IMG). We also filtered out from the data money commissions of catering, communication trainings and the production of advertising objects. We only examined procurements that were clearly intended for media buying, or mixed tenders of media purchase and pr-services, or creative/advertising commissions. The basic data table contains 1548 lines and 102,667 cells. Out of this, 898 lines and 4,494 cells remained (with the exclusion of repetitions, faulty or unsuccessful procurements and bad CPV code entries as well as data unfit for analysis) after both manual and software cleaning (Google Refine). The period of examination was between 1 May 2010 and 30 April 2014. Unfortunately, pre-2009 data referring to the period of the governments of Ferenc Gyurcsány and Gordon Bajnai could not be extracted due to the many mistakes and extremely low quality of earlier official provided information. Consequently, CRCB was only able to present comparative findings published as of 2009 (this comparative data set and corresponding findings are to be published later - Editor). A substantial comparison between the two government periods would only be possible if the state and the Procurements Office proceeded with the complete re-registration of all data starting from 2006, following at least the present practice.

|

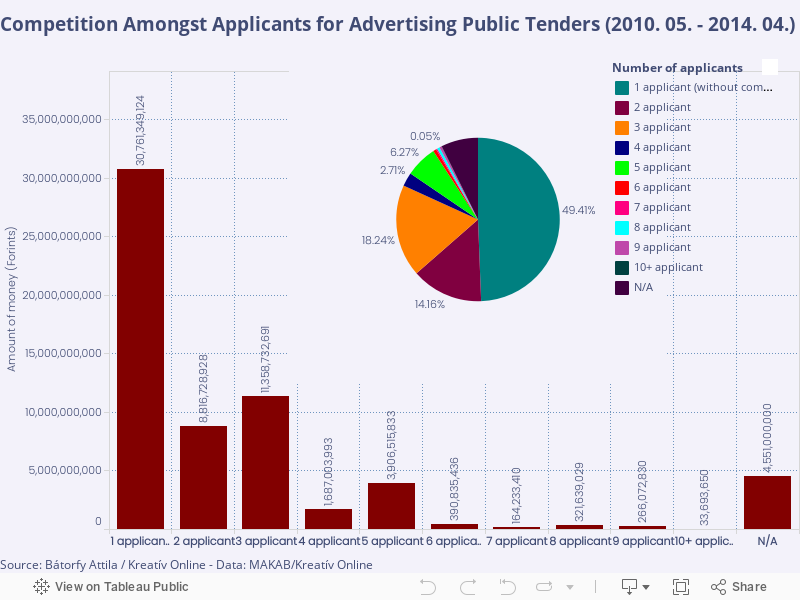

30 billion without competition

Hungarian state sector distributed a total of HUF 60,4 billion (as of now, we refrain to publishing net worth sums) during a 898 communication procurement procedures under the previous Orbán-Government. From graphs and corresponding data it can be established that the full operational administrative system has been established between the change of governments and the end of 2011, by then, key decision makers have all been replaced, and a new method of handling public acquisitions became customary. In 2012 a large scale wave of communication procurements started, and the spending only increased to unprecedented levels in 2013, the year preceding the general elections. This wave lasted up until the elections, as during the four months until the end of April 2014, the state distributed 85% of the whole 2013 amount while during the election campaign, altogether 50% of the entire amount of money spent in the whole term has been distributed.

An overwhelming majority of public procurements consisted of duties below the official threshold of procurement tenders, and consequently these commissions were not publicly announced, although its results were published in official digests. Their proportion was altogether 80.6% (724 cases), but this engulfed only 12.8% of all funds distributed (meaning a net worth of HUF 7.72 billion - all amounts of money are disclosed in net worth from now on).

The vast majority of such cases were regional, small communication commissions, at an average worth of HUF 8.6 million each. At the same time we can still talk about a real competition at these procurements, with an average of 2.66 competitors per tender. In the higher price range of HUF 25-100 million per tender, there is still a competition (with an average of 2.77 competitors per tender) but above that amount the number of applicants radically decreases with 2.05 per tender in the HUF 100-500 million price range, 1.78 per tender at commissions in the HUF 500-1000 million price range, and 1.75 per tender at commissions above HUF 1 billion. Based on that we can safely state that the more public money available at a procurement tender, the less applicants there were.

A reason for this phenomenon could be that the handling of larger sums required more specific references and experience. At the same time the fact that the average number of competitors at tenders above HUF 500 million was below 2 cannot be explained with the lack of expert agency knowledge. This number is even more interesting as although there were only 28 procurements above HUF 500 billion in the previous government term, in these procedures 65% of the total amount of public funds distributed was accessible.

It is hard to tell, what qualifies a process as a real competition, but in cases where there was a single applicant, we can clearly rule competition out. The total worth of procurements with a single applicant during the previous term was HUF 30.2 billion. Consequently nearly half, 49% of all the funds was distributed by the state sector without any competition whatsoever! As according to our view, two applicants do not qualify a tender as a real huge competition either, then if we include tenders with altogether two applicants, than we can state that the state sector has distributed 62.6% of all funds available without an essential competition, meaning little or no competition at all. In the private commercial sector, an average communication tender has 4-5 invited agencies as participants.

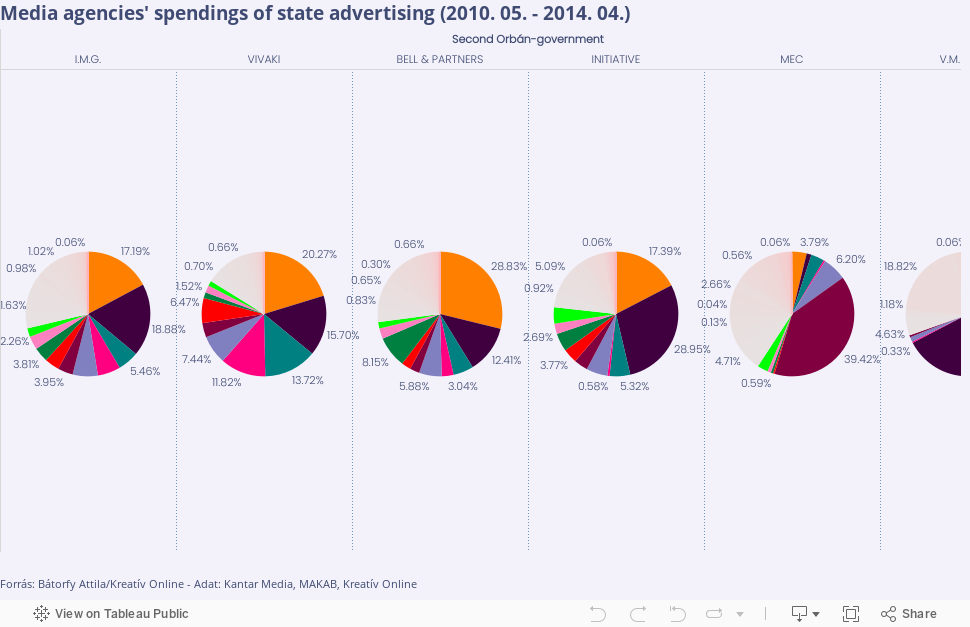

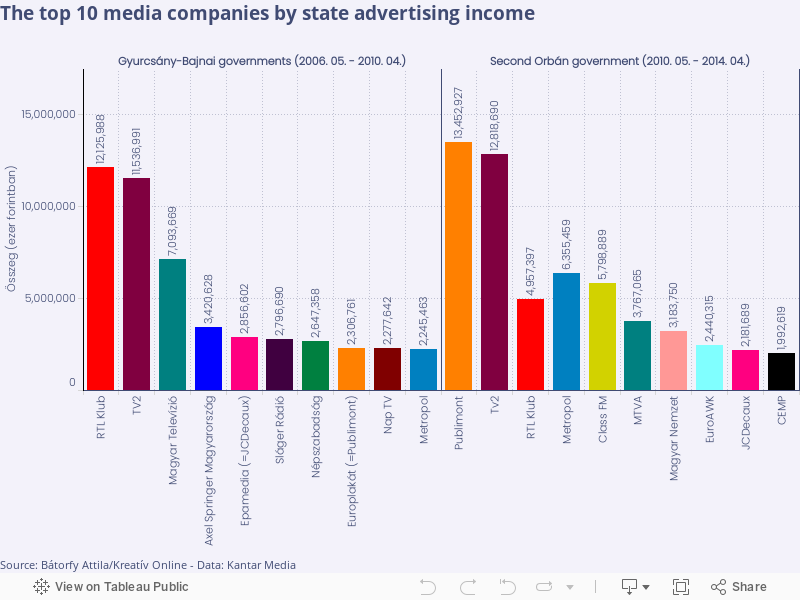

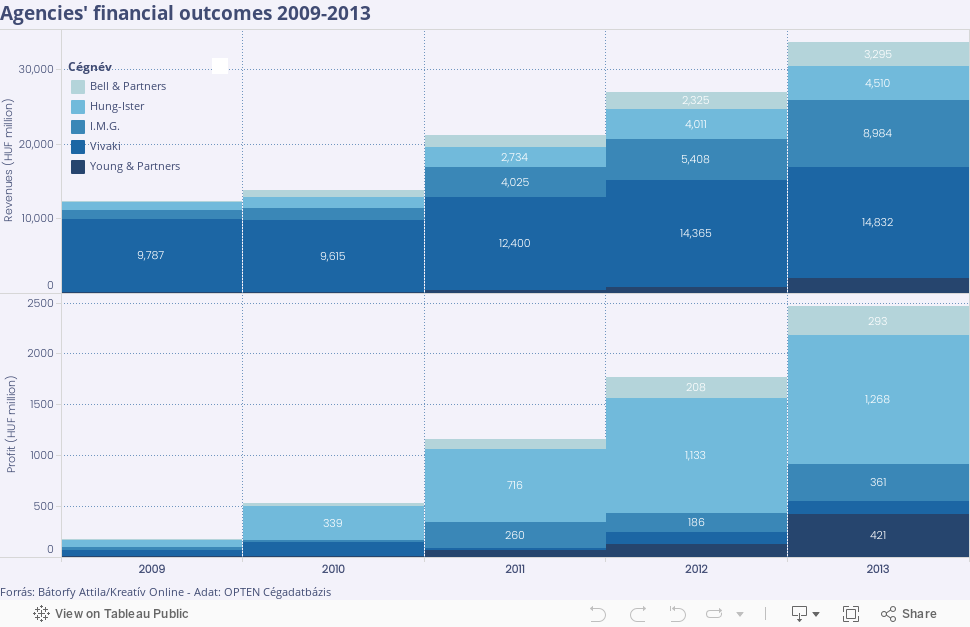

The Giant has no battle

It was already clear from the news and articles published during the previous term that the market of communication procurements has some heavyweight actors. I.M.G. Inter Media Group, Vivaki, or Bell & Partners have been mentioned quite often not only in the specialized B2B press but in major online news outlets as well. We detailed in the previous chapter what kind of personal relations network the beneficiaries have and how all of them are connected to Fidesz and its financial background. Out of the ten biggest companies using public funds we can find five where an obvious connection between the government administration and its economic supporters and the beneficiary can be revealed (such as I.M.G., Bell & Partners, Young & Partners, Hung-Ister, Théma Publishing Co.). Besides that we should mention that Mahir Group (Mahir Cityposter, Mahir/Monday, Mahir Kiállítás és Rendezvény) won a further HUF 1.5 billion. Here however we will only deal with how much money the agencies most successful during procurements won, and in what kind of competition environment they secured these funds.

As it is easily derivable from the pie chart, on the entirety of the public procurement market a supremacy of the above mentioned agencies has been developed. I.M.G. secured 30.28% of the total amount distributed, Vivaki secured 18.62% while Bell & Partners got 14.04% of the accumulated value of HUF 38 billion (total percentage of the three of them is 62.94%).

What however is even more informative then the pie chart data is that the three agencies secured this extraordinary large proportion of money during tenders with a low competition. I.M.G. won 15 procurements when it was the single applicant, while this number is 14 at Bell & Partners. Young & Partners, that also is an agency with strong connections to government circles won 9 tenders as a single competitor. In this way, I.M.G. secured 77.9% of the total amount of public tenders it applied for while this proportion is 70.43% at Bell & Partners, and 79.24% at Young & Partners. Unfortunately in one case we are not aware of the number of competitors at Vivaki, and therefore we were unable to calculate a normal value in their case.

Results published in Közbeszerzési Értesítő and Tenders Electronic Daily only provide the number of applicants only, without disclosing the names of the applicant agencies. This is why we cannot present with hard data what other agencies ran against the winners. At the same time based on known data, we can conclude as much that there were numerous procurements where the 2-3 greatest winners competed against each other.

Based on what we wrote so far, it is clear that we deal with a two-fold corruption risk factor here. On one hand, more than 60% of the whole amount distributed (including advertising-, media buying - as well as pr-commissions) was secured by three agencies (70% of it by five!), on the other hand, they either did not have to compete for the contracts at all, or they were up against each other. At the same time, there are many advertising, pr- and other media agencies operating in Hungary. Kreatív annually publishes financial results in the sector. These calculations are made taking financial data provided by 100 advertisement agencies, 25 media agencies and 60 pr agencies into account. In reality there are even more actors on the market than that.

Salient cases

Besides the data, there were many procurement tenders where the bare description of the process could raise the suspicion of corruption, or at least it was full with corruption risk elements. In multiple instances where the documented background story served with more useful lessons than the end result.

On of these was a media buying procurement announced by the National Media Authority (NMHH) in August 2012 another one was a similar procurement announced by Hungarian National Bank (MNB) in December 2012, and a third was a media buying procurement announced by the National Agency for Waste Management (OHÜ) in August 2012. A fourth such case is a tender for the utilization of advertisement space in the possession of Budapest Public Transport (BKV).

Taking above findings into consideration it will not come as a surprise that the protagonists here were I.M.G. (Media Authority, National Bank) and Bell & Partners (OHÜ). At the Budapest Public Transport tender billboard companies owned by Lajos Simicska (Publimont, Euro Publicity and EuroAWK) were the key players. As all of these stories can be consulted in detail in Hungarian by following the links, here we will restrain ourselves to only highlight acts within the stories that are highly suspicious of corruption.

NMHH-case

A procurement advising company excluded competitors of I.M.G in an oblique as well as confusing way during its HUF 1.9 billion NMHH public tender. Among parties excluded only one challenged the reasons of its exclusion yet they would have been unable to pay the established administration service fee, established as 1% (HUF 19 million) of the procurement value. The procurement advisor of the excluded company then filed a private complaint with the Procurement Authority (KH) as well as with the Office of Economic Competition (GVH). The former upheld an obligation to pay a service fee, while the latter informed advisors that they did not have the legal basis necessary to initiate an investigation. The Procurement Decision Board could have done this on its own behalf regardless, but this never happened. In this way, NMHH was only able to ask I.M.G. to offer a quote, thus the agency won the tender as a single qualified applicant.

MNB-case

Procurement results of MNB (Hungarian National Bank) with a net worth value of HUF 200 million was attacked by I.M.G. at the Procurement Decision Board, as according to them they would have been obliged to publish pricing data essential for the procurement procedure that violated the business interests of the applicant. Furthermore, they claimed that the calculation of quoted prices on behalf of MNB was unprofessional. Even though the Board eventually ruled in favor of MNB, meaning that according to them, business interests of I.M.G. were not harmed during the procurement, this verdict was already made after National Bank governor András Simor left his position, and thus the tender has been retracted before the appointment of a new management. Following that, with the governance of György Matolcsy, the MNB announced a new tender that had a so far unprecedentedly high fixed allocation of HUF 6 billion for media buying, that has been secured by I.M.G. as a single competitor.

OHÜ-case

The OHÜ public tender had an unprecedentedly short notice application deadline of three days from announcement. This already raised suspicions. The case has even been picked up by politics, with opposition party Politics Can Be Different (LMP) filing a report in the case with a charge of embezzlement. Following that there was a single applicant on the tender, Bell & Partners that won the contract. The Procurement Decision Board started an investigation into the case on its own initiative against OHÜ, and established that the announcement of the tender was unlawful. The announcer was fined to HUF 5 million, yet the results of the tender have never been retracted.

BKV-case

The tender to utilize advertising spaces of the transport company were ab ovo suspicious as this was not advertised as a procurement procedure. Besides, the announcement had such conditions that made only Simicska’s companies, Publimont, Euro Publicity and Euro AWK eligible and able to apply - running against each other. One applicant billboard company, Peron that has been excluded from the tender initiated a procedure against BKV at the Procurement Decision Board, and another excluded party Epamedia also joined the lawsuit. During the legal procedure it was additionally revealed that Márton Viszkei from the department of commerce at BKV took part in the announcement of the tender. Viszkei was also the owner and CEO of Bell & Partners (former owner of Euro Publicity). In the end, the Board decided that BKV’s announcement was unlawful and a procurement procedure is needed to be initiated. BKV started over the procedure in May 2013, their procurement plan proposed to the Budapest capital assembly however repeated all the restrictive conditions of the previous tender, adding some insensible points as well. After Kreatív published on the day of the assembly decision that the plan has elements restricting competition, the assembly retracted the procurement plan on 29 May, with a reasoning that there were too many questions arising. A procurement tender consequently has never been announced.

Such a manner of analyzing communication procurements is only sufficient in itself to highlight major anomalies. Even though major procurement winners profoundly enhanced their net worth income and profits in the previous government term, according to their company data procurements in themselves are not especially profitable to them, as they are working with a very low agency fee charged. This is especially the case with media purchases, where we really are only talking about cash flowing through these agencies, as they are winning money especially to spend it somewhere else instead of the state. Therefore the most apparent and important question with such brokerage/mediatory deals is where does the money go from there.

Part IV.

DISTRIBUTION OF STATE ADVERTISING (05.2006 - 04.2014)

Database provided by: Kantar Media, Adex, state sector

Data collection method: Kantar Media Collection (methodology can be accessed here)

Is this data free to access? No.

Systematization of data: In Excel, can be filtered by cycles, by years, by months, by owners, by media + by amounts, and by purchased airtime or space

Number of records used: 7600 lines (629,730 cells)

Period of examination: May 31 2006 - 30 April 2014

Visualization software: Tableau Public

Can anyone download the data for a double check? We are not allowed to disclose the database of Kantar Media to a third party.

Most important findings:

- 51.66% of all state advertisement ended up at commercial media owned by businessmen close to the government, or commercial media loyal to the government as well as at the public media.

- This picture is a bit misleading as if we examine the numbers referring to different types of media, then we find the following proportions at government friendly outlets: daily print: 68.23%, weekly and monthly print: 21.75%, radio: 86.06%, television: 51.33%, out-of-home ads: 74.12%, online: 0%. This means that in those types of media where businessmen close to the government hold interests, or where there are media outlets loyal to the government, the state sector, and its preferred media agencies have spent the overwhelming majority of public advertisement money.

- This practice can be proven to be functional already during the governments of Ferenc Gyurcsány and Gordon Bajnai, but such a level of disproportionality and of the market-distorting effect of the state was not yet characteristic.

- The earlier claim surfacing in the media agency and sector according to which the distribution of state advertisements is the most beneficial with regards to its price/value proportion cannot be upheld. Advertising in the pro-government media is extremely expensive. Even though there are elements of the portfolio that could not be avoided, but favoring pro-government outlets is significant even in cases where no market metrics would dictate such a behavior, or the accessible data even contradicts such decisions.

| Methodology of data collection |

As in our earlier writings about state advertisements, here we also have pruchased data from market research company Kantar Media. Advertisement spending data collected by Kantar Media is recognized and used by the whole advertisement- and media market and other media outlets (like HVG and Index) and researchers (Mérték Media Monitor, Whitereport) also consult them for similar works. Spending data is calculated using official advertisement tariffs published by media outlets, meaning that it does not include discounts provided for certain advertisers. To put it in a simple way: these prices correspond to how much we are supposed to pay if we simply walk in from the street to buy a poster. Kantar Media documents advertisements on every media outlets of all media types on a daily basis, preparing a summary based on official tariffs/rate card prices. These data consequently is not suitable to determine how much money an advertiser really spent at an outlet, it is barely enough to establish tendencies and proportions. According to a calculation formula widely accepted on the market, advertisers usually spend 40-50% of the official tariffs/rate card prices in the given outlet. Besides the database purchased from Kantar Media contains the amount of advertising space or in the case of radios and televisions the amount of advertising airtime, purchased. From these two set of data it is possible to draw more or less realistic conclusions. For multiple reasons, Kantar Media does not measure certain media outlets that are important parts of the market, that usually are owned by pro-goverment businessmen, such as Hír TV, Lánchíd Radio, Mahir Cityposter and Echo TV. In the core database of Kantar Media we were forced to make certain amendments for the sake of an effective comparison between the two government terms. Europlakat is being shown under the name of its purchaser, Publimont in the whole period, and the earlier existing Epamedia and other members of its holding are indicated under the name of their present owner, JCDecaux, and with the sum of their annual advertisement income. On the online media market we indicated results of the earlier existing Index.hu Zrt. under its present owner, CEMP in the whole period. We considered data from the following pro-government media outlets regardless of the government term:

|

Introduction

Distribution of state advertising is one of the most controversial topics on the Hungarian media market. Even though the state is not a major advertiser on the domestic market, in summary it is to be regarded as an important factor in the income of media companies. Distribution of state advertising is a very effective tool of intervention into the financial outcomes of certain media companies. As a significant part of Hungarian media companies was counting on advertising income from the state and changes in this distribution system automatically generate losers and winners. We do not subscribe to the idea that the state should not allowed to communicate. There is a number of state duties, services and projects that are indeed worth calling attention to, but a sensible line should be drawn in this. The most important aspect of state advertising spending however should be a strict observance of the price/value ratio, as well as to be the most effective and the cheapest, targeted communication tool. Since April 2010 barely any of these requirements could be realized, but on the other hand, capitalization of the pro-government media empire resulted in the empowerment of the media portfolio. In this way, by 2013-14 more and more cases and campaign-situations occurred when a pro-government media selection could achieve about the same numbers as any other selection of media.

An opportunity to compare state sector advertising practices to that of the commercial sector would be a very significant addition to the demonstration. On the out-of-home/billboard media market (earlier outdoor media market) we were able to demonstrate a significant difference based on Kantar Media data between advertising logic of the two sectors. The clearest situation would be if we would be able to separate campaign messages to barely the same kind of target groups to compare different media selections. Based on that, we would be able to establish differences and similarities between commercial and state advertising practices. Such a detailed data on commercial advertising however could only be known to the advertisers and their agencies and even if we would possess such data we would not be able to publish it as we would violate business secrecy. And even if we would possess such information we would have to take the fact into consideration that commercial advertisers often make favors to incumbent governments with advertising more in the pro-government media as before. Such a conformity has been confirmed to us by numerous radio market experts following the change of governments.

Market weight of the pro-government media became especially strong by the 2014 general elections. Elements of the portfolio became inevitable not only for state, but for commercial advertisers as well. At the same time, the 2014 situation is by far not evident. A significant assistance on behalf of state administration and lawmakers was needed to this, furthermore the observable disproportionality of state advertising practices after 2010. So when we draw the conclusion that the distribution of state advertisement is disproportionate than we should also keep it in mind that parallel to that the state was aiming to influence media market power structure using administrative tools.

Catching up at the finish line

During the second Orbán government, the state sector spent HUF 80.46 billion on advertising according to rate card prices. This was HUF 3 billion less than in the preceding Gyurcsány-Bajnai era. It can be observed in both government terms that - as we have already seen at the procurements - governments need some time until the new administration take the seats and gets familiar with its operational method. At every change of government spending usually hats for a small period of time, but the level of decrease was smaller in the beginning of the terms of Ferenc Gyurcsány and Gordon Bajnai in office, as they were following an earlier similarly Socialist-Free Democrat administration, and that was not a real profound change. The most significant year of that term was 2008, this was when the newly established National Development Agency (NFÜ), a government organization responsible for the handling of EU funds started a large scale communication strategy.

Media purchase spending of the second Orbán-government in contrast started to unfold much slower only to surpass the record year of 2008 by some measures in 2013. In that year, state sector rate card price spending was altogether HUF 26.7 billion. This shows for a trend that is similar to the one concluded from the already presented procurement graphs meaning that with the general elections closing up state sector started to rapidly increase its communication spending in the media. In the monthly breakup of data, it can be clearly seen how during the election campaign, and especially in the month preceding the April general elections the government spread the money around.

In the breakdown by types of media we can see which types of media were favored in the two subsequent government terms. While Socialist-Free Democrat government preferred nationwide television channels and daily newspapers, the Orbán-Government communicated through billboard posters, radio stations and the internet.

The breakdown by advertisers demonstrates which state advertisers were the most active in which government term. We routinely filtered out the smallest spenders and will only show those who are profoundly significant in state advertising or where there was a remarkable change in the habit of spending funds in the comparison of the two terms.

We can see, that during the Gyurcsány-Bajnai governments the ministries were running most of the state advertising immediately followed by the National Development Agency, Szerencsejáték Zrt. (National Lottery), State-debt Management Center (ÁKK) and the National Chief Police Constabulary (ORFK) as top advertisers. During the the second Orbán-government ORFK spent much less on advertisement with NFÜ and Szerencsejáték also losing some of their significance (while remaining important advertisers), ÁKK retained its role yet at the same time a number of strong new actors entered the stage of big spenders. Examples for the latter are Hungarian Postal Services, Hungarian Electricity Works, Ministry of Public Administation and Justice - Prime Minister’s Office, Erzsébet-vouchers program, Media Authority, public media company MTVA, Magyar Turizmus, Student Debt Center, and the Hungarian National Bank.

Everything points to one direction

The bulk of our readership is probably most interested in which media outlets the state sector eventually preferred to spend the most money at, meaning what was the amount of public money reward received by certain media owners?

There were media outlets receiving more money under this or that government, the the question always was whether it was an effective strategy for the state sector concerning the price/value ratio, or were there better uses of the public money earmarked for communication spending?

This question generates a lot of tension, especially when those who think that it is an obligation for the subsequent governments to reward friendly media with state advertisement and other things are a majority on both sides of the political arena. As we will see - and will deal with it in detail in the next chapter - it was a recurrent topic during the second Orbán government as well that this was about more than the question of how the government provides a little compensation for media actors adopting government policies without any criticism. The structure of the whole system was more about how friendly media owners can extract a larger profit from the public money flowing to their companies.

In the following pages we will present different media types separately. There are four graphs corresponding to each media type, these can be accessed by clicking on the tabs.

Graph 1. presents how much a certain media outlet received per month in state advertisement money under the two government terms. Separate colors mean different media outlets, the size of the circles is proportional to the amount of money received. When there was an extraordinary media market occurring, like a change of owners, we signified this on the graph.

Graph 2. presents the same thing as the previous one, only the annual amount borken down to purchased advertisement space, following the trends. The thickness of the graph is proportional with the sum of the spending/number of purchased advertisement space.

Pie-chart 3. presents how large proportion of advertiding money a certain media outlet received in percentage during the two government terms under examination. The size of the circles is proportional to the share of state advertising money received.

Graph 4. presents how much money was received by which media outlet from which advertiser during the two subsequent government terms. The size of the circles is proportional to the amount of money.

We think that graphs, charts, and pie-charts present a by-and-large accurate picture of how state advertising were distributed, as well as about the identity of beneficiaries and about what was the cost of advertising at which outlet. We wish you a successful browsing and filtering!

In the following paragraphs, we will offer a separate analysis of each type of media. Even though the graphs often talk for themselves, but we will also summarize our major findings and the most significant circumstances raising numerous questions in connection with each of the beneficiaries for the sake of better understanding.

Daily newspapers

Total official tariff spending: Gyurcsány-Bajnai administration (Gy-B): HUF 17.9 billion/4 yrs, Second Orbán government (O2): HUF 15.1 billion/4 yrs.

Largest share: Gy-B: Népszabadság 14.54%, O2: Metropol 42.05%

Largest advertiser: Gy-B: NFÜ HUF 4 billion, O2: Szerencsejáték HUF 3.16 billion.

Total share of pro-government papers: Gy-B (Népszabadság, Népszava) 21.09%, O2 (Magyar Nemzet, Magyar Hírlap, Metropol): 68.23%

Note: In the database of Kantar Media, Népszava appears through two separate publishers: Editorial, and Néspszava Publishing. We combined their numbers in the purchase years.

As many people think that daily newspapers (and television) constitute the entirety of the media market, it is of symbolic importance besides numerical how the state distributes advertisements on the daily newspaper market, including most importantly political dailies, that are traditionally considered to be strongly affiliated with a political party in Hungary.

We can clearly see that leftist-liberal newspapers received more state advertisement under the Gyurcsány-Bajnai administration. At the same time these ratio is more or less corresponding to the number of copies sold and the size of readership. In sheer contrast to this, the second Orbán government did overturn this - in our view rational and reasonable - structure, and in effect discontinued state advertising in Népszabadság and Népszava, while enhancing the share of Magyar Nemzet to 21% within the segment. Even Magyar Hírlap, that is not even audited by the Hungarian Association for the Observation of Circulation (MATESZ) for its small readership received a larger share of state advertising with 5.12% than Népszabadság’s 3.77% and Népszava’s 0.63% combined.

If we only consider the four daily political newspapers with a nationwide circulation than a political alternation between the two governments is apparent. During the Gyurcsány-Bajnai governments the proportions were as follows: Népszabadság 45.74%, Magyar Nemzet 28.09%, Népszava 20.6%, Magyar Hírlap 5.57%. And during the second Orbán government the situation was: Magyar Nemzet 66.69%, Magyar Hírlap 16.21%, Népszabadság 11.94%, Népszava 5.16%. While during the Gyurcsány-Bajnai there is a potential problem with the proportions, at least papers were ranked based on their readership and the number of copies sold. Under the second Orbán government, exact market metrics ceased to matter.

At the same time, none of these papers had such a large share than Metropol, that had received 12.53% of state advertisements during the Gyurcsány-Bajnai era, and that grew to 42.05% under Orbán. In Metropol, state advertisers started to spend a lot of money when in July 2011 the paper has been acquired by Károly Fonyó, a businessmen belonging to the stock-yard of Lajos Simicska. Even though Metropol is an inevitable object on the daily newspaper advertising market substantially increasing the number of its copies over the years, this amount of share can be classified disproportionate.

The total share of the whole pro-government daily newspaper portfolio of 68.23% contradicts market logic. The assumption obviously is not that these newspapers - together with others - would be unsuitable to reach targeted groups that the government aims to reach through its communications. The problem is more like with the disproportionality, and prices. If the statement that agencies winning procurement contracts will spend this money where the price/value ratio is most beneficial for the state proved to be true, than this money would have been spent on the same wider target group where prices are lower, and the process is more accountable.

A possible explanation could be if the readership of pro-government media outlets is especially designated as a political target group in the media plan, meaning that specifically beneficial results, projects and messages of the government would be meant to sent exclusively to these papers. Let’s not forget that this could be a possible tool to keep the electorate intact. From that point of view the step of using state apparatus media budget for that could be considered logical albeit unethical.

Activity of the advertisers broken down to papers show another interesting pattern. It is of course natural that the Prime Minister’s Office, that is in effect the government prefers pro-government daily newspapers for its advertisements. It is much harder to rationalize however why Szerencsejáték chose the low readership and low access Magyar Hírlap for advertisingt during the second Orbán government, or how come that Hungarian Electricity Works (MVM, also meaning MVM Partners, and the Paks II development media campaign) were so fond of Magyar Nemzet that they provided them with 60% of their whole newspaper budget?

Consequently two parallel interests make public money to flow into the same direction on the newspaper market. The government, in charge of running the state sector simultaneously aims to communicate to its own electorate, wanting to explain numerous measures heavily attacked by the opposition to them, or to keep them enthusiastic.

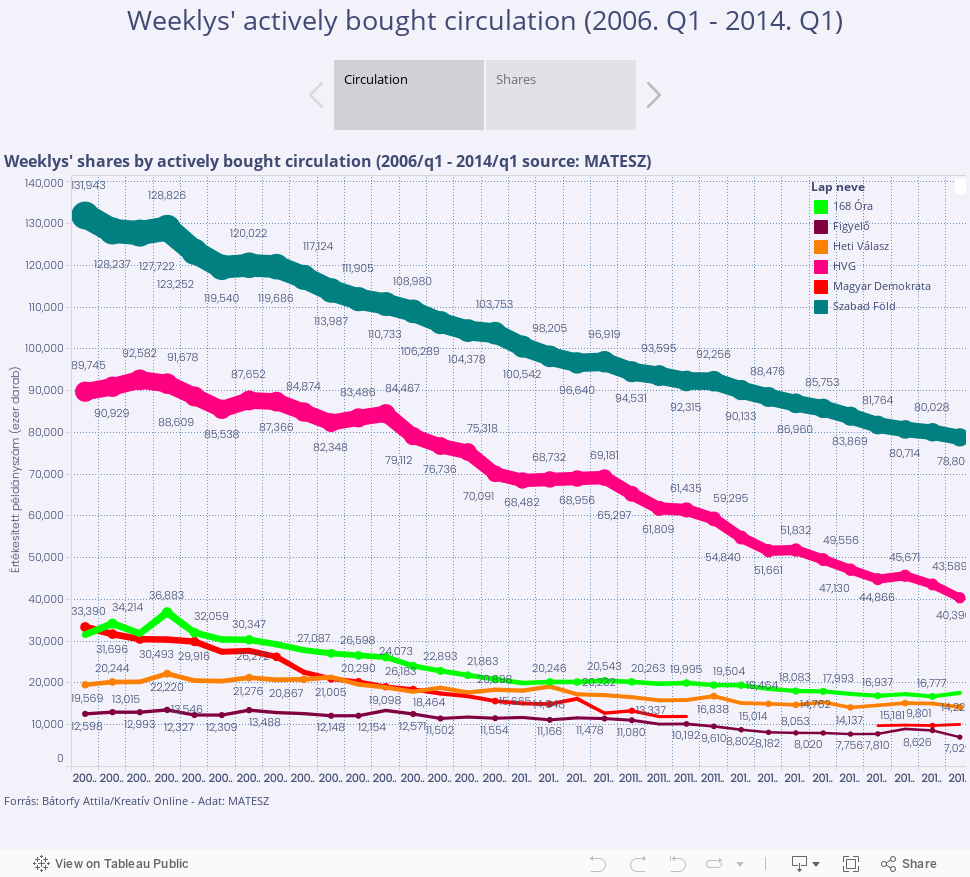

Weekly- and monthly newspapers

Total official tariff spending: Gy-B: HUF 7.73 billion/4 yrs, O2: HUF 5.53 billion/4 yrs.

Largest share: Gy-B: Szabad Föld 8.55%, O2: Heti Válasz 20.76%

Largest advertiser: Gy-B: NFÜ HUF 870 million, O2: Magyar Posta HUF 526 million.

Total share of pro-government papers: Gy-B (168 Óra, Szabad Föld, Magyar Narancs) 16%, O2 (Heti Válasz): 27.76%

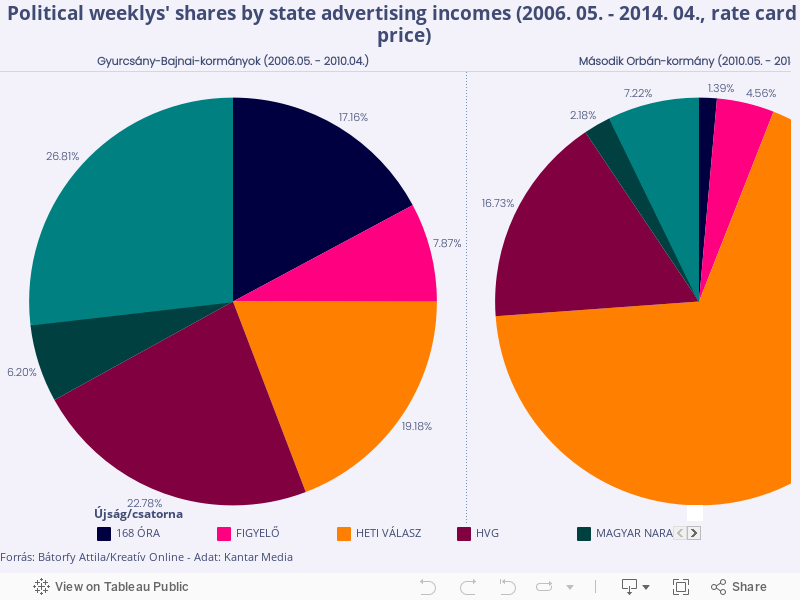

The market of weekly prints is virtually the only type of media where the domination of pro-government outlets did not happen. This however is only the case at first glimpse, as in this segment the selection is much more diverse, and there is only one weekly that is in pro-government hands, Heti Válasz.

If however we further proceed to break down weeklies into a sub-category of political weeklies, than the situation changes entirely. Most debates erupt around which weeklies to be filed under what party, we consider Szabad Föld leftist-liberal because of its owner, and Magyar Narancs as well as 168 Óra, due to their political endorsements. And, even though we ourselves strongly disagree with such an interpretation, but following public opinion and for the sake of preventing unneccessary debates we filed HVG and Figyelő under the same category. Comparing these five papers to the advertising market share of Heti Válasz the proportions will profoundly change after we took state advertisement income ending up at the six weeklies as 100%. In this way, it can be established that the summarized share of state ads in the first five weeklies during the Gyurcsány-Bajnai era is 80.82% (Szabad Föld: 26.81%, HVG: 22.78%, 168 Óra: 17.16%, Figyelő: 7.87%, Magyar Narancs: 6.2%) while Heti Válasz received 19.18%. Contrary to that, during the second Orbán government combined share of the five weekly papers considered to be leftist was 32.08% (HVG: 16.73%, Szabad Föld: 7.22%, Figyelő: 4.56%, Magyar Narancs: 2,18%, 168 Óra: 1.39%), as opposed to 67.92% at Heti Válasz.

It is worth considering whether state advertising proportions were by all means proportional to the market weight or not under the Socialist-Free Democrat coalition governance. We think these state ad-distribution proportions to be more or less corresponding to real market weight and readership-reach. We would however not that the printed copies and accumulated share of these papers can easily be utilized by the Conservative right to support their theory of a “leftist-liberal media prevalence” on the weekly print market. As opposed to this the 67.92% state advertising share of Heti Válasz under Orbán is a clear disproportionality considering both the number of copies sold and readership/reach of the paper.

It is worth noting that that political weeklies constituted a third of the combined income of the market segment in the period, weekly women’s, automobile and other magazines published by Sanoma and Axel Springer in total were able to present a very strong share under both governments, and this could be supported by the market metrics.

Disclaimer: Our publisher, Professional Publishing Hungary (PPH) received HUF 12.525 million in state advertising during the Gyurcsány-Bajnai era, and HUF 2.859 million during the second Orbán government.

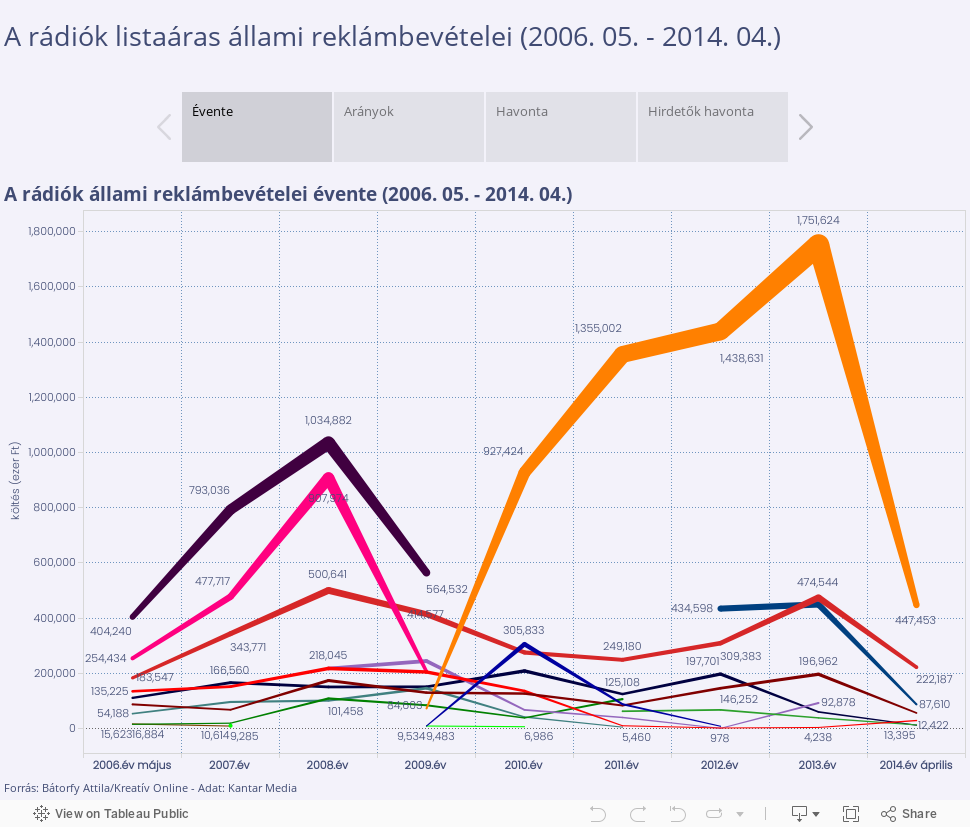

Radios

Total official tariff spending: Gy-B: HUF 9.8 billion/4 yrs, O2: HUF 10 billion/4 yrs.

Largest share: Gy-B: Sláger Radio 28.56%, O2: Class FM 57.56%

Largest advertiser: Gy-B: Szerencsejáték HUF 4.15 billion, O2: Szerencsejáték HUF 2.63 billion.

Total share of pro-government papers: Gy-B (Klub Radio, Hungarian Public Radio) 23.95%, O2 (Class FM, Music FM, Hungarian Public Radio): 81.13%

In order to understand advertising incomes on the radio market it is necessary to recall the gravest case suspicious of corruption showing the entanglement of political and economic elites better than ever before, the nationwide commercial radio frequency tender of October 2009. This is were two radios, Sláger and Danubius ceased to exist giving way to Class FM and Neo FM - in a way that was later pronounced to be unlawful at court. Consequently the radio market turned on to the finish line of change of governments in a situation like this, only to face even more intervention with market environment and the government jointly finishing of Neo FM, the radio with connection to the Socialists by November 2012. Afterwards, Class FM, owned first by Zsolt Nyerges, and later by Lajos Simicska became the single nationwide radio, and state advertisements started to rapidly pour into it. After Neo FM ceased to exist its frequency has not been advertised for a tender by the Media Authority but automatically gave it to Hungarian Public Radio. Meanwhile a new radio, connected to Zsolt Nyerges through its new owner, Music FM has been founded that started to receive state ad money even in the absence of official data on its audience. Local and regional frequencies have been routinely acquired by Lánchíd Radio and Catholic Radio, owned by Simicska’s businessmen, Gábor Liszkay and Zsolt Nyerges.

After the discontinuation of Neo FM both market and state advertising sectors thought that its end has been caused by the inability of advertisers to sustain two nationwide commercial radios following the economic crisis. Besides this it is interesting however that since then, Class FM and Music FM were both able to increase their turnover and profits mostly due to the influx of state advertising money. This means that the state contributed to a single-actor market and later to the founding and the financial success of a new radio by its one-sided distribution of funds. On the radio market, the background story itself is more thoughtful that the numbers, as the latter should not come as a surprise. Class FM received 57.56% of state ads, Music FM received 9.56% and Hungarian Public Radio received 14% during the four years of the second Orbán government. As long as it existed, Neo FM achieved 2.26% of the share. State advertising incomes of Lánchíd Radio are unknown to us, because as we have mentioned earlier, Kantar Media does not audit them in its database.

If we combine these results with the fact that the commercial airtime of Class FM, Neo FM and local radios is being sold by Sonitus Media, that has been acquired from I.M.G. by Metropol-owner Károly Fonyó who belongs to Lajos Simicska’s interest group, than we can observe a centralized control of the radio market segment by the state that is unprecedented.

Televisions

Total official tariff spending: Gy-B: HUF 36.25 billion/4 yrs, O2: HUF 24.97 billion/4 yrs.

Largest share: Gy-B: RTL Klub 33.44%, O2: TV2 51.33%

Largest advertiser: Gy-B: Szerencsejáték HUF 13.5 billion, O2: Szerencsejáték HUF 5.8 billion.

Television market began to get interesting in terms of state advertising when in mid-May 2013, HVG.hu published that TV2 could become a crown jewel of the Simicska-Nyerges media empire. In the following months, many people, including ourselves, were trying to find out who will buy TV2 from the marketplace. Besides Simicska, Swedish Modern Times Group, operating cable entertainment channel Viasat surfaced as another potential buyer as well as other pro-government businessmen, and even Chinese investors. The involvement of Fidesz was not entirely surprising as TV2 chief director Zsolt Simon was known for his good connections to the governing party. This is why it was so surprising that he and Yvonne Dederick, so far financial manager became the new owners after the management buy out. In practice, this meant that Simon received a 2018 deadline to pay the full acquisition price of approximately HUF 15-20 billion to the previous owner, German Pro7Sat1.

Apparently, this was the moment when state advertising funds started to interest everyone. It became clear early on that a fundamentally loss-making could not be made profitable in such circumstances. According to an article also appearing at HVG.hu certain media agencies were approached by pro-government businessmen to require them a major restructuring of commercial advertisements in favor of TV2. After the inauguration of the second Orbán government plans for an advertising tax have been announced. This was a proposal about which even the government admitted later what everyone else knew anyway: namely that it was directed against the largest commercial television, RTL Klub with the help of many amendments, and in way that TV2 will not be affected by it in 2014. In fact according to data that has been published so far, RTL paid 80% of all advertising tax revenues into the central budget.

In light of all this, numbers are not especially surprising. From the data it can be seen that the state really started to beef up its advertising spending at TV2 over the course of 2012, but only a few exceptional months could have been established. In reality it is mid-September 2013, namely the middle of the selling process of the television when state advertising media agencies started to ship larger amount of money to TV2, the government/Prime Minister’s Office, Szerencsejáték, Hungarian Postal Services and the Hungarian National Bank were extremely active in this process.

Out-of-Home

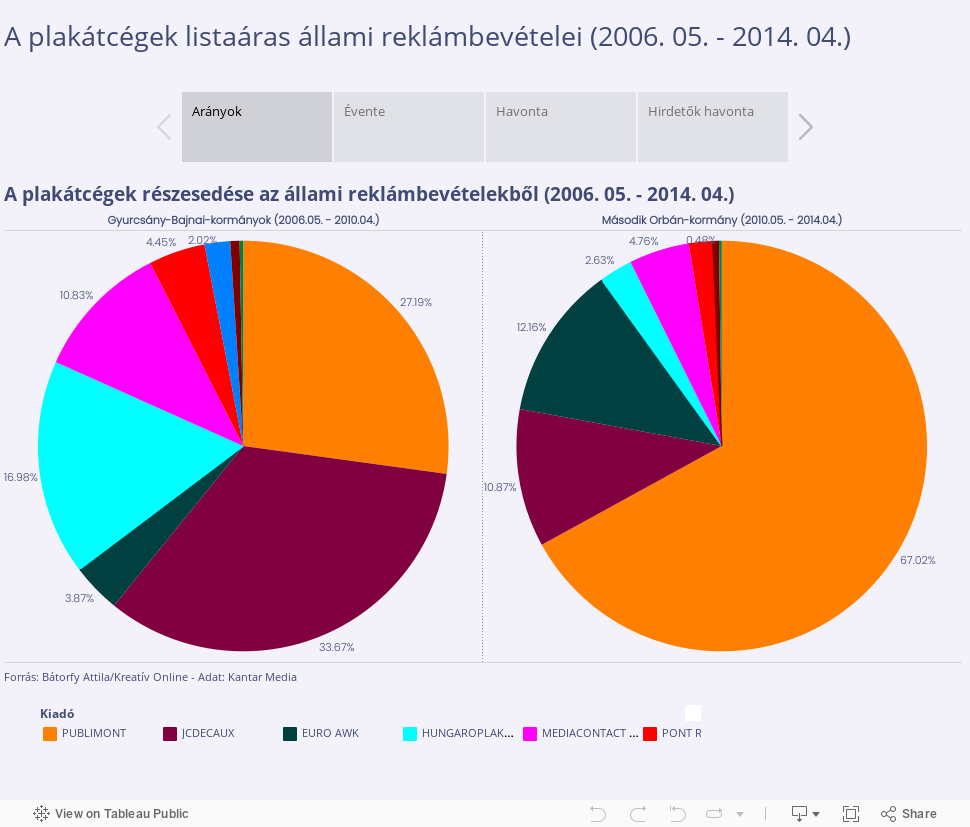

Total official tariff spending: Gy-B: HUF 8.5 billion/4 yrs, O2: HUF 20 billion/4 yrs.

Largest share: Gy-B: Epamedia (JCDecaux) 33.67%, O2: Publimont 67.02%

Largest advertiser: Gy-B: ORFK HUF 1.5 billion, O2: Szerencsejáték HUF 3.29 billion.

Note 1: Epamedia is included under the name of JCDecaux as a result of a change of owners in the whole period.

Note 2.: Kantar Media collects and estimates data from billboard companies based on self-assessment.

Public space media, or the billboard market has been covered extensively in our earlier articles. What was worth knowing about them, has already been published at Kreatív. In addition main data did not radically change by April 2014. This is a type of media where an ideological purpose cannot be identified, as you cannot manipulate which posters to come across, they are all over the streets.

On the billboard market, Fidesz interests are traditionally very strong. After the privatization of Mahir, it came into the property of Lajos Simicska as Mahir-Cityposter, later to be joined by Károly Fonyó’s EuroAWK. The real change in the power structure favoring the holding has been achieved by the acquisition of Euro Publicity, the real big player Europlakát renamed to Publimont. This made them a major domestic competitor to Epamedia - later JCDecaux, a French-owned multinational billboard giant. After the change of government in 2010, the state started to help to pave the way for Simicska, with a law erroneously referred to as “Lex Mahir”. The bill, penned by Zoltán Schváb, a former director at Simicska’s construction company Közgép, who at the time was working at the Ministry of National Development ousted a significant Spanish-Hungarian competitor with traditionally good connections to the Socialist party, ESMA from the market by forbidding them to use electricity pylons for advertising purposes. The ESMA vs. Hungarian State court case is presently being waitlisted at the European Court in Strasbourg. The bottom line however was one less competitor to worry about.

The process that in the meantime started to unfold on the billboard market is hard to be called anything else than sheer profiteering financed from state money, that made the largest bargain not exclusively of the segment but of the whole media market, out to Publimont.

A little before the 2010 change of regimes, besides ESMA, Epamedia and Hungaroplakát were considered to be companies with stronger or weaker connections to the Socialists or the Free Democrats. This could well be the case, however data does not show that this would have been a key factor in the distribution of state advertising. These billboard companies profited from state advertising proportionally to their market weight.At that time, Epamedia (JCDecaux) had 33.67% of the shares, Publimont that was the second biggest of the market received 27.19% of the state ads, while Hungaroplakát had 16.7%. The change of governments however brought about a profound change on the market. One hand, during the Orbán government official tariff prices of state spending on out-of-home ads rose from HUF 8.5 billion to HUF 20 billion. This means that the Orbán government deemed it especially important to increase the presence in this segment of the media. Proportions developed as follows: Publimont 67.02%, EuroAWK 12.16%, JCDecaux 10.87%. And this is with excluding Mahir-Cityposter that is not audited by Kantar Media. Companies close to the government (Publimont, EuroAWK) achieved a combined share of 79.18% altogether during this government term.

At state advertisers, it can be observed that while during the Gyurcsány-Bajnai era, major state organizations using billboards included ORFK, and to some extent Szerencsejáték and NFÜ, then after Fidesz s coming to power a number of state companies suddenly started to allocate large sums of their budget to out-of-home advertising. Not only Szerencsejáték raised its spending to four times more, but State-deficit Management Fund, Magyar Turizmus, Prime Minister’s Office, NFÜ, Hungarian Postal Services, Media Authority, and Hungarian Electricity works all did the same. It is as if they would have followed a secret spell, out of the blue, they decided that it is worth communicating more on billboards, especially on the billboards of Publimont.

In addition, this change was not cheap. When in the past years we have prepared analyses on the out-of-home market, then experts always emphasized when compiling media-mixes that they are working with the best price/value ratio. Based on this data we do not find this claim to be founded, as Publican is by far the most expensive - at least it seems so after consulting official tariff prices traced back by Kantar Media. This of course as well mean that Publimont provides the largest discounts, but this claim cannot be proven. The situation is even more complicated, as official tariffs are public at every other type of media (meaning they could be accessed online) than this is not the case at the out-of-home market.So for example a procurement tender could be won in a way that the agency, putting all confidence in Publimont or in any other company, promises as much as 60 or 70% discount on the tariff prices, only that nobody else is aware of these tariffs. As a side not we should remark that before the 2014 general elections only out-of-home advertising had not been made more difficult by the amended election law, meaning that this became the only type of media, where billboard companies have not been obliged to publish their official tariffs and fixed prices to political parties.

After the change of governments, public advertisement became the element of the Simicska-Nyerges-Fonyó portfolio that was making the most profit (see the next chapter of our study), and this is partially due to the fact that such a nationwide network could be operated with a relatively low added value, and with less workforce, while contractors will put posters out in an especially low price.

Online

Total official tariff spending: Gy-B: HUF 2.96 billion/4 yrs, O2: HUF 4.55 billion/4 yrs.

Largest share: Gy-B: Origo 28.4%, O2: CEMP (Index) 43.58%

Largest advertiser: Gy-B: Prime Minister’s Office HUF 0.67 billion, O2: Szerencsejáték HUF 1 billion.

Note 1: Kantar Media changed the name of Index to CEMP during the Gyurcsány-Bajnai government.

Note 2.: Kantar Media collects and estimates data on online advertising based on self-assessment.

The relative independence of online media was never due to the ownership structure but to the fact that editorial offices were able to operate independently from or contrary to owner expectations for a very long time. The ownership structure in the online media market is not ideal either.